Before the iPhone launched in late 2007, Apple was trading consistently at a P/E ratio above 30. Here is a table for the P/E ratio on each Friday’s closing price from May to August, 2007. The iPhone launched on June 29, 2007.

| Date | P/E Ratio |

| 5/23/07 | 31.5 |

| 5/30/07 | 31.6 |

| 6/6/07 | 34.1 |

| 6/13/07 | 33.7 |

| 6/20/07 | 34.6 |

| 6/27/07 | 33.6 (2 days before iPhone launch) |

| 7/11/07 | 37.2 |

| 7/18/07 | 34.6 |

| 7/25/07 | 34.3 |

| 8/1/07 | 33.3 |

| 8/8/07 | 34.2 |

| 8/15/07 | 30.2 |

Apple was not super powerful but it was not doomed either. It was a time when the iPod was dominant and the Mac was still alive. iTunes re-wrote the rules of the music industry and debate was raging whether Apple should be considered a media company. Platforms were not its strength but Steve Jobs showed he was still able to distort reality.

These good times did not last. The first year of the iPhone was a period of minimal contribution from the new category with Apple still largely valued on the basis of the iPod. The predictions of failure for the new communications product, especially given its high price, were legendary. It wasn’t until 2008 that the iPhone began accelerating and making a meaningful contribution to the bottom line.

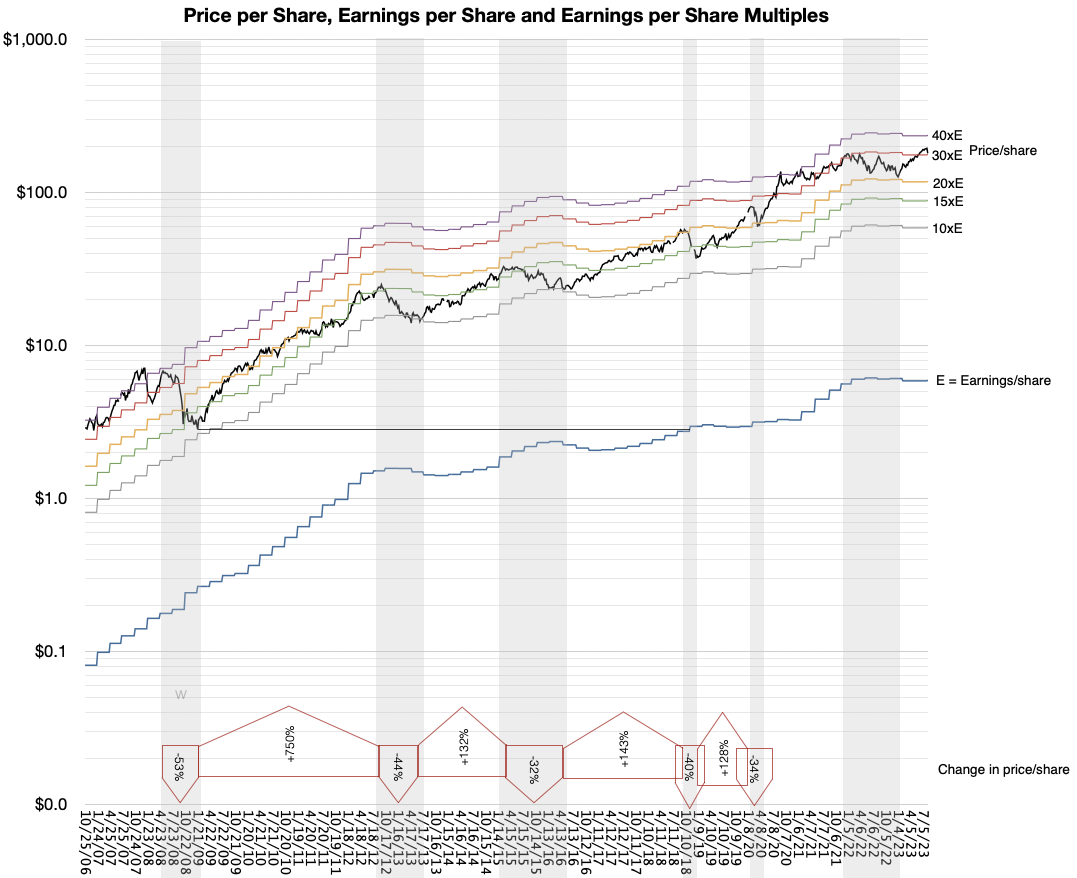

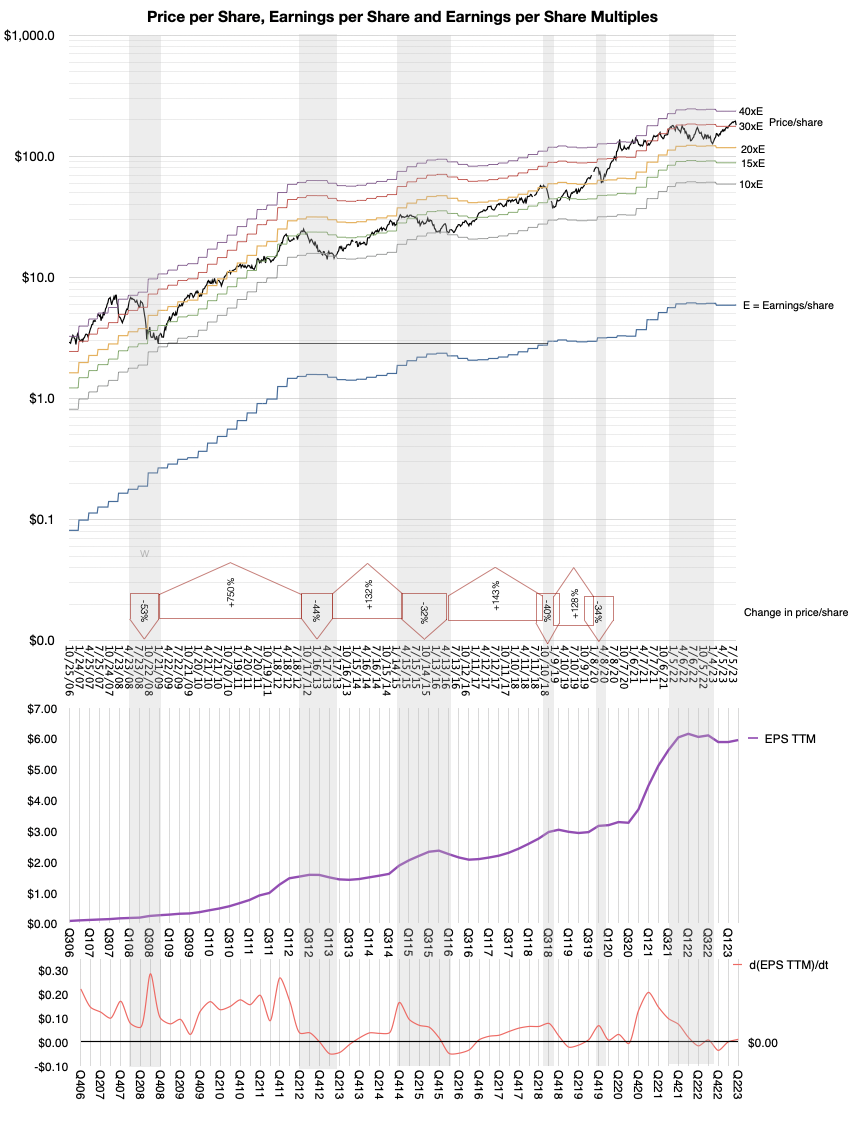

It was then, in late 2008, that Apple’s valuation broke. The P/E ratio fell from above 30 to nearly 10. The following graph shows the catastrophic 53% share price collapse coupled to the triple digit surge in earnings which led to the P/E ratio tanking.

[The graph shows earnings per share for the trailing 12 months (blue line) and 10x, 15x, 20x, 30x and 40x that value (colored lines). The share price is the black line. The share prices are sampled every Friday. The graph is notably logarithmic. The grey shaded areas are periods of significant contraction. The percent drops/increases during these periods of contraction/expansion are shown in the annotation arrows near the bottom.]

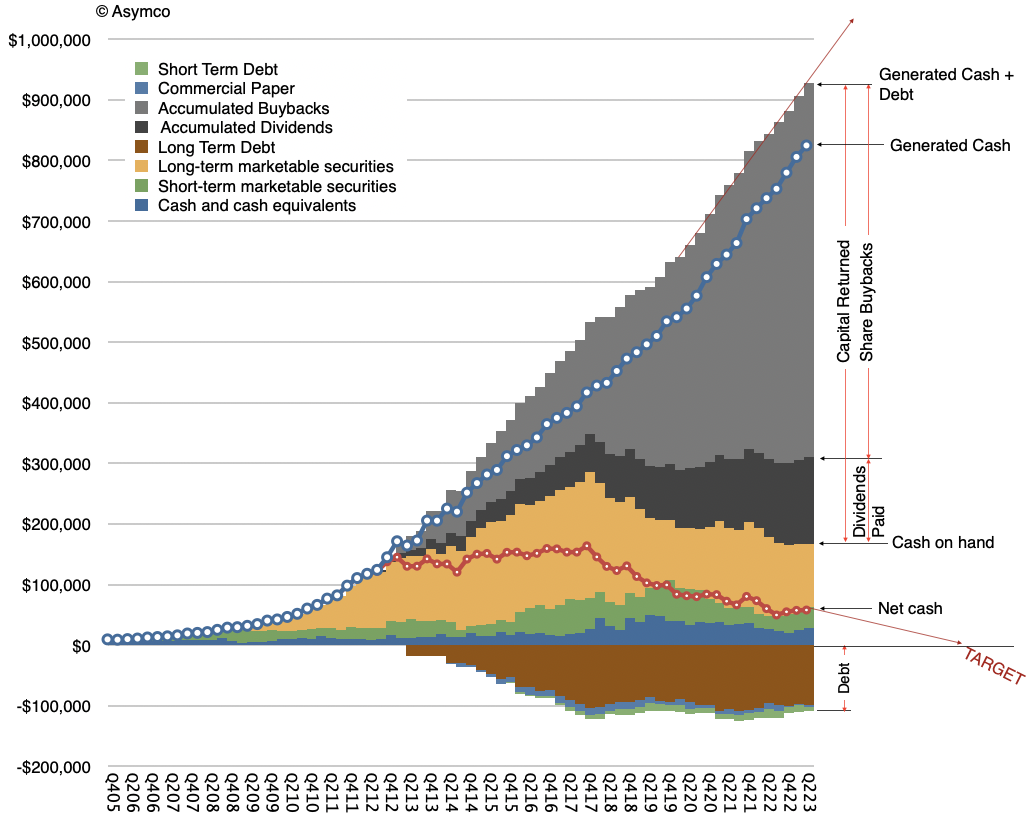

The valuation remained broken for 12 years, between late 2008 and late 2020. This period being, arguably, the most remarkable wealth creation event in history of business. For evidence see the following graph showing the amount of retained earnings returned to shareholders building inexorably toward one trillion dollars. This is not share price appreciation but cash returns. [If you have evidence of a larger wealth-creation event do let me know.]

The creation of $800 billion of shareholder wealth at fire-sale share pricing.

As I explained throughout this period, motivation to dispose of shares which create immense wealth is explained by the fable The Goose That Laid the Golden Eggs but the question some are asking now is whether more wealth can still be created, and if so, can we expect Apple’s valuation to collapse accordingly?

I should note that during the long, dark years of wealth creation, other technology companies such as FaceBook, Amazon and Netflix, Google (so-called FAANG) and Microsoft enjoyed far higher multiples than Apple, sometimes 3x higher. This was not seen as abnormal by analysts because those companies were always assumed to have higher growth potential, with a diverse portfolio of opportunities while Apple’s growth was perpetually in its past, based on one product.

Paradoxically perhaps, since the Covid-19 pandemic Apple shares have enjoyed P/E ratio roughly equivalent to the other tech companies. For instance, peaking at 42 in January 2021, the P/E ratio has averaged about 27.5 since then. Simultaneously, diversified companies such as FaceBook (now Meta) and Netflix collapsed due to serious business model flaws (based on single sources of income) and Google (now Alphabet) and Amazon have slowed growth and are facing anti-trust scrutiny. Having lost any presence in mobile computing Microsoft has become entrenched in enterprise, finding new businesses in cloud and (possibly) generative AI. As a result of these reversals, the contrast between Apple and the mega-cap cohort has become fuzzy.

So back to the question: does it make sense to price Apple in the 30x P/E or should it go back in the gutter at 10 to 20?

I would argue that the big change in perception hasn’t been the surge in earnings during Covid (see graph below). The big change is the realization that Apple is no longer about to go out of business.

How could Apple not be going out of business?

Remember that a P/E ratio in the teens is a clear signal from the market that the company is a questionable “going concern”. This is parlance indicating doubt that the company will continue in its present form..

What has changed since 2020 is that even though there were a multitude of crises—from war to pestilence—the eggs kept coming. Perhaps, perhaps, Apple was not doomed after all. In that time it managed to create 1 billion customers. Perhaps having 1 billion customers was a positive outcome. Perhaps counting iPhones during a single quarter was not the only way to value the company. Perhaps having 1 billion satisfied customers made it viable. Perhaps having 1 billion satisfied and loyal customers returning every year was interesting. Perhaps having 1 billion satisfied wealthy customers meant the end is not around the corner. Perhaps having 2 billion active devices in use was sustainable. Perhaps providing services to 1 billion customers using 2 billion devices delivered through 1 billion subscriptions made some sense. Perhaps having all this data in a linear graph made it predictable?

Perhaps. Though Apple provided updates on these figures regularly, the questions everyone asked were still on unit shipments (which Apple stopped providing.) While Services grew at double digits and 70% margins the questions from analysts on conference calls persist on the iPhone and currency or production “headwinds”. Perceptions take time to change. They are still changing.

Maybe at this point it’s time to agree that Apple’s end will not come through being easily replaced by the competition (first Windows then Android, etc.) but by having access to its markets restricted. Being the only American company to have cracked the China puzzle, it’s surely vulnerable there. And please don’t mention India.

Apple is no longer doomed because it’s too weak. It’s doomed because it’s too strong.

It seems that it’s not too hard to believe the end is still near.